Fund Managers’ Letter

4th Quarter 2025— Jacques Berghmans et Félix Berghmans

Introduction

As we start a new year, we find it interesting and very often humbling to look back at what we wrote 12 months ago. Financial predictions tend to age more like milk than fine wine, and decades in the financial markets have taught us that flexibility is crucial. An excellent outcome is often avoiding big mistakes rather than getting everything right. That said, our last newsletter of 2024 focused on artificial intelligence and the freshly elected Trump administration, which were certainly two of the key themes of 2025.

Our cautious optimism and our advice to look beyond the tech-heavy American stock market also aged well. 2025 was one of the first years, in recent memory, when the rest of the world significantly outperformed the US, especially when taking dollar depreciation into account. AI continued to massively impact markets, though the best performers were for once not listed on the NASDAQ but found in South Korea, Taiwan and, in some cases, decades-old European industrials.

2025 Market Performance

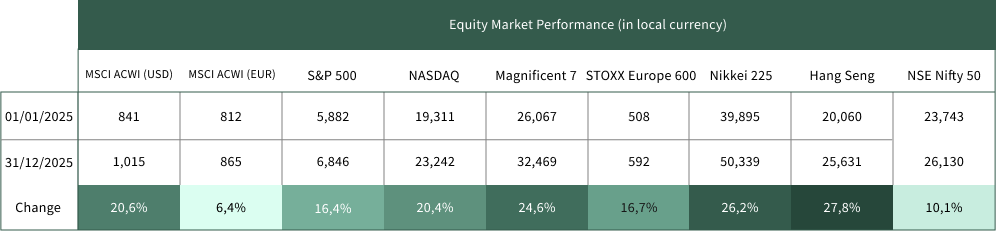

2.1 Global Equity Markets

Nearly every major equity market delivered positive performance in 2025:

• The MSCI All Country World Index was up more than 20% in US dollars (unhedged) though only 6.4% in euros

• The S&P 500, the most important index in the US, was up 16.4% in US dollars

• American technology companies continued to outperform with Nasdaq and Magnificent Seven up 20% and 25% respectively

• The European market delivered excellent performance, up 16.7% for the year

• North Asia was the best performing region: Japan +26%, Hang Seng +28%, KOSPI +76% in local currency

Source: Bloomberg

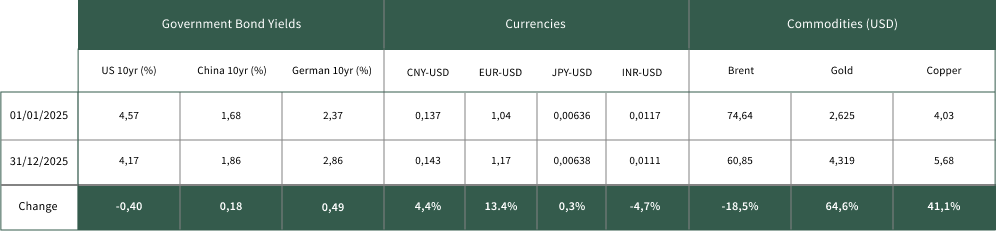

2.2 Currency & Commodity Dynamics

While 2025 was a very good year for the stock market, it was also marked with significant volatility in currencies and major commodity prices. Other than the aforementioned volatility, the global economy was generally solid with low inflation, stable interest rates and no major financial crisis.

Source: Bloomberg

Gold and copper prices went up significantly. The gold price was driven by speculation on accelerating inflation and general macro-economic uncertainty. Gold has been very volatile historically and supply and demand dynamics are nearly impossible to forecast. Most of the world's gold sits in vaults and could quickly flood the market as it did during the last bear market in the nineties. Copper prices have been mainly driven by tight supply and increasing demand from electrification and the AI boom. Correlation with industrial activity means copper is not a good hedge for investors as it will likely go down with the stock market during a recession.

Source: Bloomberg

2.3 Interest Rate Environment

Global interest rates stayed relatively stable with Europe converging with the US as lower inflation enabled the US Central Bank (the 'Fed') to cut its reserve rate. While inflation in Europe was stable, it stayed at a higher level than prior to the COVID pandemic and prevented further cuts by the European Central Bank ('ECB'). The likelihood of interest rates falling significantly from current levels is low. With inflation stabilising at 2 to 3% year-on-year in the United States and Europe, close to their long-term historic trend, maintaining long-term interest rates around 3% in Europe and 4% in the United States makes macro-economic sense. Returns for investors will therefore depend on earnings growth, with asset classes like fixed income and real estate not likely to benefit from dropping interest rates like they did between 2000 and 2022.

Key Lessons from 2025

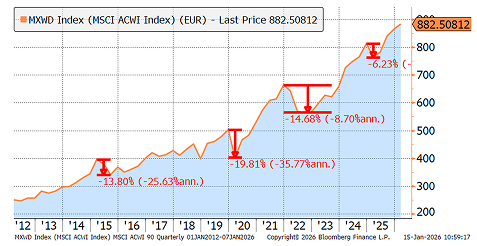

3.1 Don't Panic and Sell on Bad News

2025 was the first year of Trump's second administration and it didn't disappoint in terms of surprises. The biggest shock for investors came in April 2025, when the American administration imposed unilateral trading tariffs on most nations in the world. Stocks, the US debt market and the US dollar were in free-fall for a few days until the US administration started to retract some of the most outlandish measures. This mini-panic in April shows that avoiding panic-selling is crucial when investing, as global markets tend to rebound quickly and strongly. As we can see on the graph above, similar panics happened in 2015 during the European debt crisis, in 2020 during COVID, in 2022 when Russia invaded Ukraine, all followed by quick recoveries of the global stock market.

Source: Bloomberg

3.2 AI's Global Footprint: Winners Beyond NASDAQ

Artificial intelligence remained the major value driver, but the biggest winners were mostly outside the United States.

In semiconductors, the best performers this year were Asian companies, like SK Hynix, the large South Korean memory producer, and Samsung Electronics, another leader in memory chips.

AI models continue to evolve at breakneck speed, improving after each iteration. At the beginning of the year, the Chinese AI model DeepSeek emerged as a very strong contender, built at a fraction of the cost of US models, which rocked the NASDAQ for a few days. In November, Google/Alphabet released Gemini 3, a new model that surprised most investors positively and led to a significant re-rating of the stock, making Google/Alphabet one of the best performing large technology stocks in the US this year. The best way to gain exposure to this investment theme is through a passive tracker, as extremely rapid technology evolution makes it very difficult to know which AI model is going to be the winner of tomorrow.

The AI boom has also started to have a significant impact on more traditional sectors of the economy, mainly related to electricity production, given the energy required by data centres. Some of the best performing stocks in Europe in 2025 were traditional industrial companies, like Siemens Energy, which saw their business boom driven by new power plants and network projects.

3.3 The World Continues to Progress

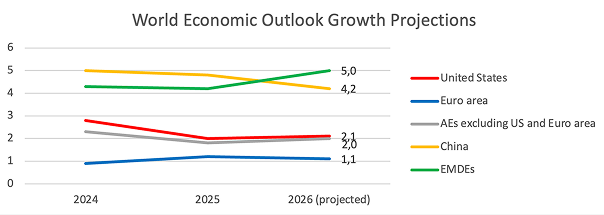

Macro-economic conditions remained good across the world with global economic growth proving resilient. In a recent blog, World Bank economists observed that since the end of the pandemic in 2022, the global economy has repeatedly defied expectations, consistently delivering better than expected growth. This outperformance was mostly driven by the US economy until 2024, but was broader based in 2025, with advanced and emerging economies outperforming initial expectations.

Source: World Bank

2026: Risks & Opportunities

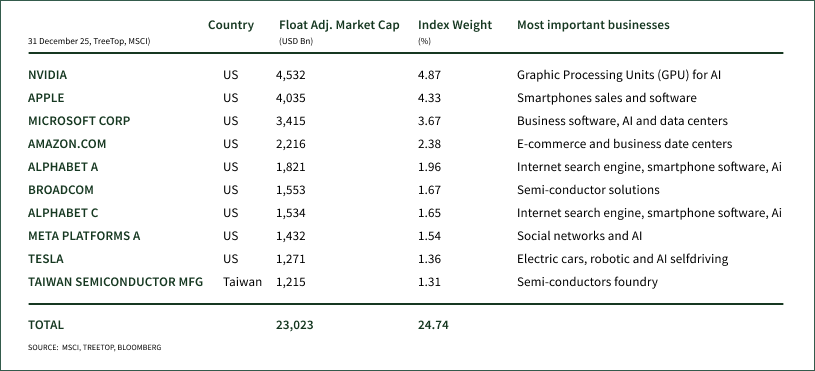

4.1 Index Concentration Risk

At the end of 2025, the top 25% of the MSCI ACWI, the most used benchmark for global equity investing, was in ten technology stocks, nine of them being American and one Taiwanese (Taiwan Semiconductor Mfg or TSMC). Except for Apple, all these ten names are heavily exposed to artificial intelligence, ranging from graphic processing units ('GPUs') for Nvidia (4.9% of the index) to data centre leasing for Amazon (2.4% of the index) to AI software for Microsoft (3.7% of the index).

Some regional indices are not any better, with for example the MSCI Emerging Markets nearly 12% invested in TSMC, the largest semiconductor producer in the world and a beneficiary of artificial intelligence. The third, fourth and fifth largest investments in the emerging market indexes (Samsung Electronics, Alibaba and SK Hynix) are also heavily dependent on AI.

Although the advantage of market capitalisation-weighted indices is their strong tendency to follow the momentum effect, allowing investors to profit from rising stock markets at a lower cost, the downside is that such indices systematically increase exposure to the largest and best-performing stocks. As leadership narrows, this mechanism concentrates risk in a small number of companies, sectors or countries. During periods of market overheating and speculative bubble formation, they overweight overvalued companies and therefore can suffer significant losses during market corrections.

Japan is an interesting historic precedent. In 1989, Japan reached roughly 45% of the MSCI World Index. Global diversification became a single-country bet. When Japan corrected, global benchmarks carried the drawdown and then their allocation to Japan lived with a 40-year long hangover.

Source: Bloomberg

The dot-com cycle repeated the same pattern through sector concentration. At the March 2000 peak, the world's largest companies included Microsoft, General Electric, NTT Docomo, Cisco, Intel, Lucent, Deutsche Telekom and NTT, a list dominated by the investment cycle of the time. What followed was not a short shock. It was a multi-year reset. The MSCI ACWI had barely recovered by the 2008 financial crisis when it plunged again, resulting in 12 years of paltry returns for investors.

Source: Bloomberg

4.2 Valuation Divergence: Cheap Stocks Exist

While some sectors and regions have become expensive, there are opportunities if you look carefully. Stocks outside the United States trade on 14x forward PE (MSCI ACWI ex-US), in line with the valuation of the last twenty years. Stocks in the US (MSCI US) have become more expensive, now trading on 26x forward PE. Valuation levels are still lower than in the post-COVID stock mania of 2021 and the dotcom bubble in the late nineties, but they are not the bargain they were ten years ago. Cheap US stocks exist and the country, despite all its problems, still has fantastic entrepreneurs, but careful selection is needed.

Source: Bloomberg

4.3 Earnings Momentum Is Shifting

Since 2022, the US market delivered the best earnings growth, followed by Europe and finally Asia. In 2025, all three regions delivered solid earnings growth with Asia bouncing back the fastest, growing 28% since its bottom at the beginning of 2024.

Source: Bloomberg

Our Approach

5.1 The Case for Discipline

Historically, skilled managers could mitigate some of the index concentration problems by doing two things that indices cannot do: valuation discipline (refusing to follow the crowd into the most expensive leaders) and capital reallocation (shifting exposure toward neglected segments).

In theory, that toolkit remains valid. In practice, the active-management industry has become structurally incapable of delivering it reliably, in global large caps, for most investors. In any given year, there are always a few managers who outperform, but very few can do it consistently over longer periods of time. Global stock picking is like competitive sport: very few winners, and most don't last long.

While the global stock market remains the best way to grow wealth over time, global indices have become more concentrated, with the risk that a bubble would drag market-cap weighted indexes down. Most active managers have a disappointing track record and there is no guarantee that they will do better in a crisis.

5.2 Our Convictions

These dynamics have shaped how we think about equity allocation. Our approach favours rules-based discipline over stock-picking intuition, diversification across styles and regions over single-factor bets, and regular reassessment over set-and-forget positioning.

In practice, that means:

- Using quantitative methodologies designed to deliver diversified equity market exposure while reducing dependence on the most crowded leaders

- Accepting that no single approach wins in all environments; therefore, building from a short list of complementary strategies

- Reviewing these strategies regularly, reassessing whether the environment remains consistent with the conditions under which each strategy historically earned its return premium

The details vary by client. What doesn't vary is the principle: exposure to global equity markets without blind dependence on the names that happen to be largest today.

Conclusion

Investing in stocks is not without risks and markets will always have corrections. Our approach is designed to mitigate these risks without eliminating them. Alongside market-cap weighted indices, we use quantitative strategies grounded in free cash flow fundamentals and shareholder-friendly capital allocation. The combination aims to reduce concentration in a handful of mega-cap names while capturing opportunities across regions and market capitalisations.

Thank you for your trust. We remain available for any questions.

Jacques Berghmans & Félix Berghmans

Legal Disclaimer

The information contained in this document is for general purposes and does not take into account the investment objectives, financial situation or specific needs of an investor. This document should not be given to a US investor (as defined in US regulations). This document is based on sources that TreeTop Asset Management SA (the "Company") believes to be reliable and reflects the views of the managers of the Company.

This document is for information purposes only and does not constitute investment advice or a product offering. The Company accepts no liability, directly or indirectly, for the use of the document information.

Data showing past performance and trends are not necessarily a guide to future performance or developments. Data & Information as of 31st December 2025. Published by TreeTop Asset Management SA, a UCITS Management Company licensed pursuant to the provisions of Chapter 15 of the Luxembourg Law of 17th December 2010.