Fund Managers’ Letter

2nd Quarter 2026 — Jacques Berghmans et Félix Berghmans

Q2 Market Performance

Most financial markets delivered good performance during the quarter with global equity markets rebounding strongly from their April low, when the conflict in Iran began. While the conflict caused energy prices to increase significantly, and oil prices remain at elevated levels, the world economy is relatively stable. There was no significant oil shortage, global credit spreads are tight and inflation remains under control. A positive surprise came from significantly better corporate profitability boosting stocks higher.

Equities

SOURCE : BLOOMBERG

SOURCE : BLOOMBERG

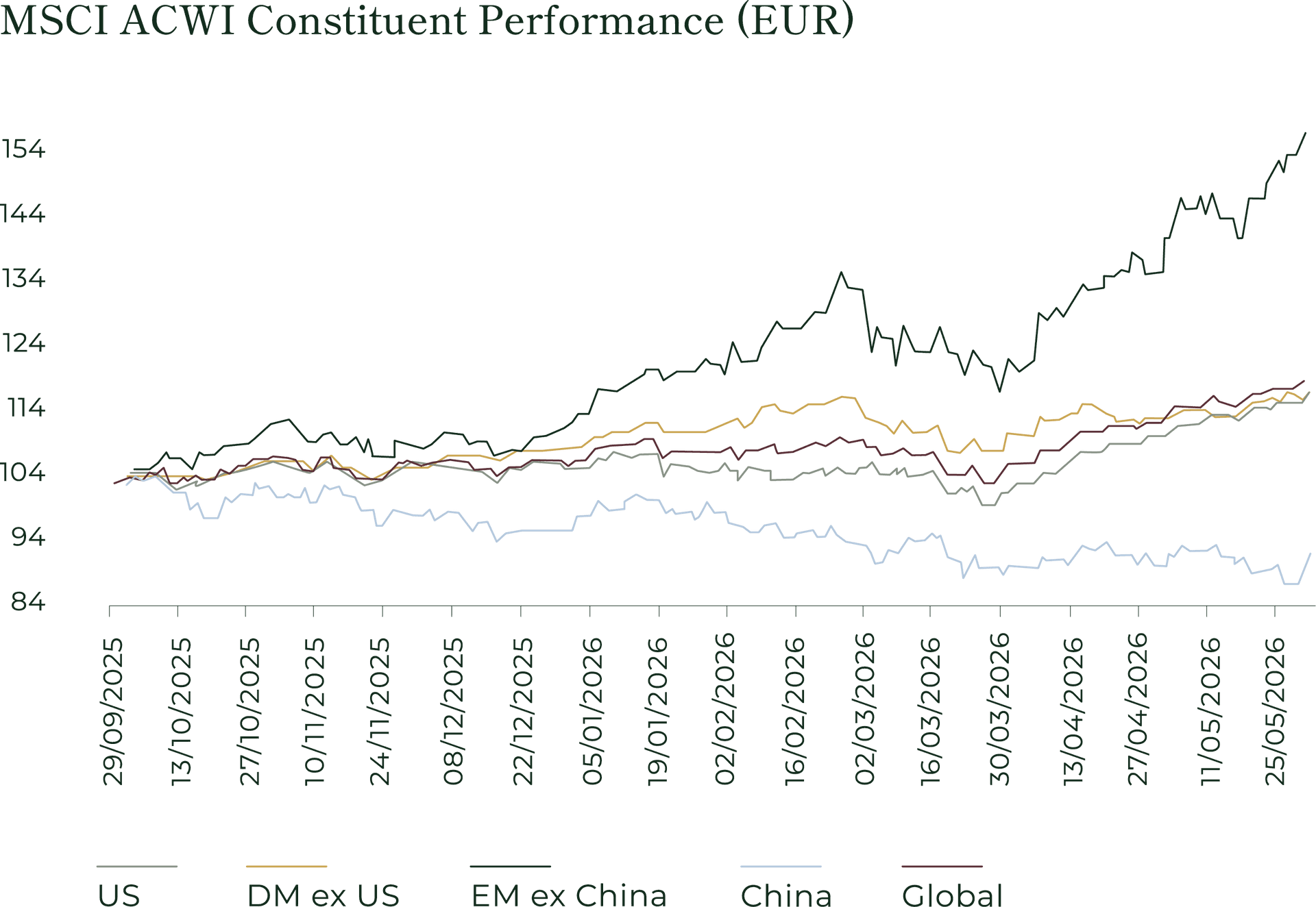

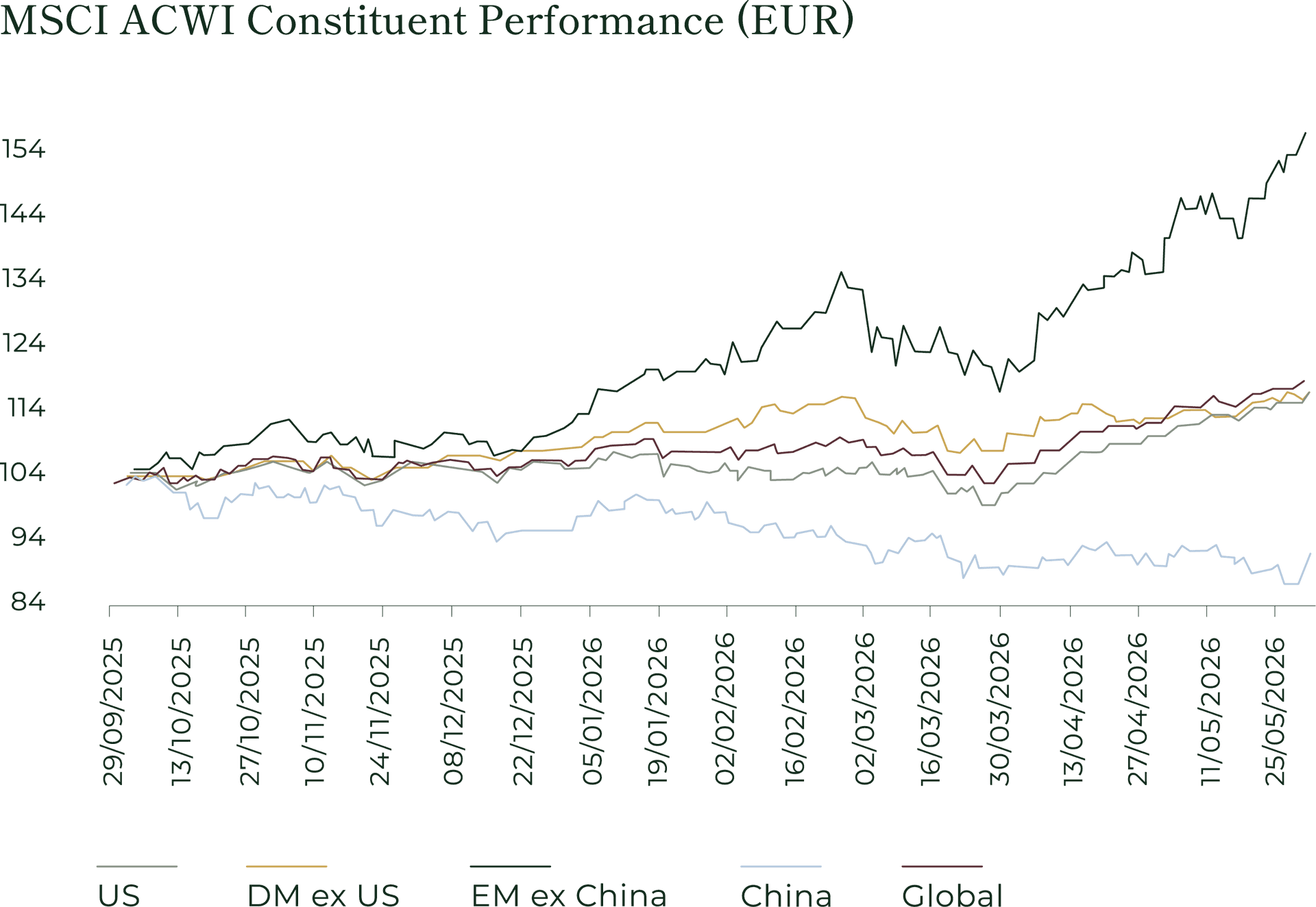

MSCI ACWI. The global benchmark recovered strongly over the quarter as recession fears receded. The chart above, which rebases each region to 100 at the end of September 2025 (in euro terms), tells the more interesting story: the headline recovery masks a wide dispersion between regions. Emerging markets excluding China led decisively, pulling away from the pack from February onwards, while Chinese equities were the laggard and the only major bloc to end the period below where it started. Developed markets, including the US, clustered together in the middle, recovering their early-year losses but delivering far more modest gains than emerging markets.

¹ The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation lost profits) or any other damages. (www.msci.com).

Macro-economic situation

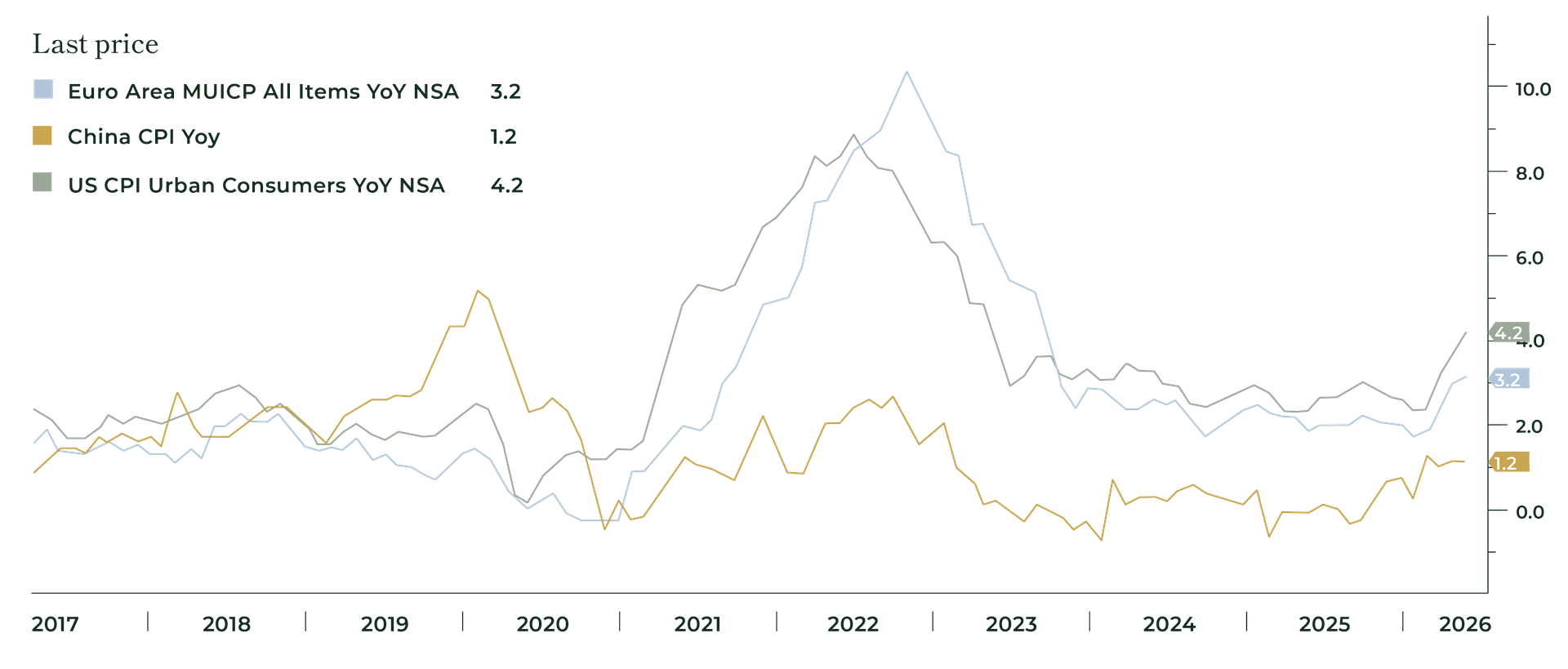

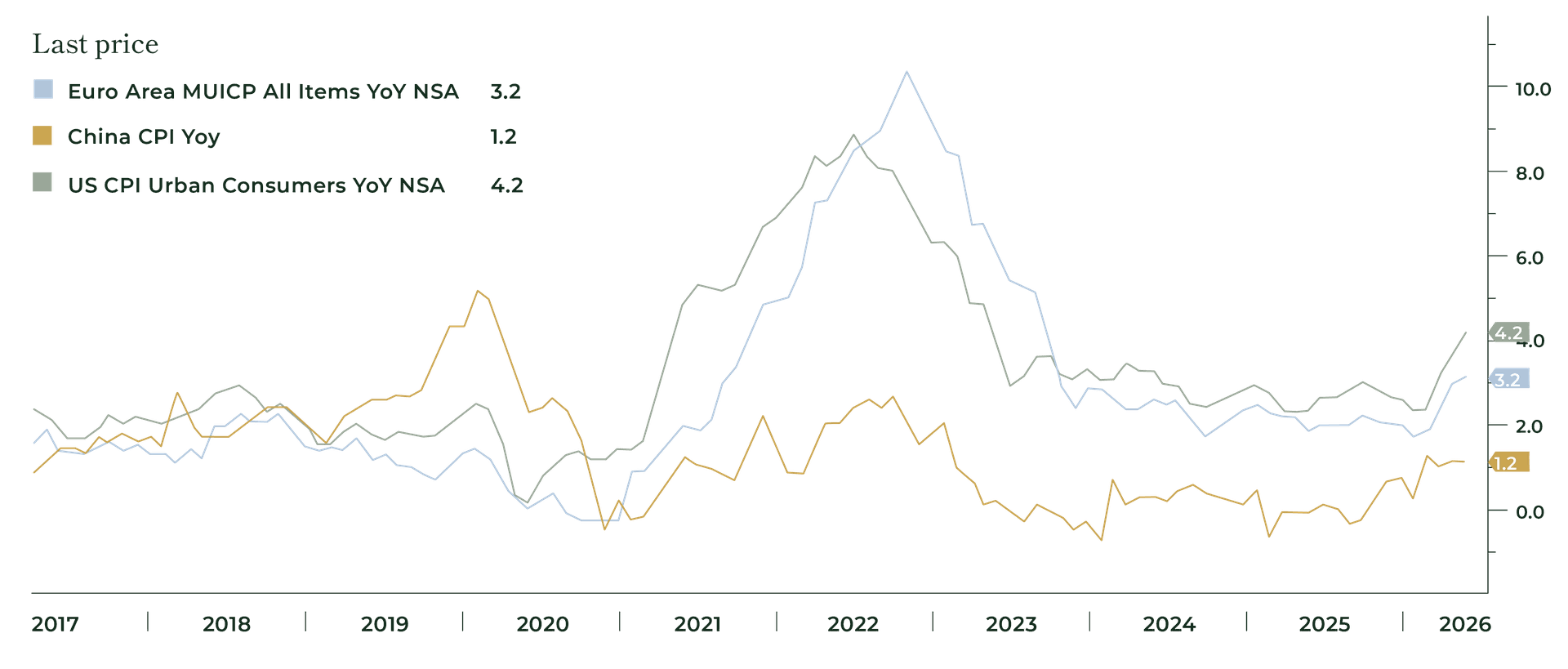

Overall, while the conflict in Iran did lead to much higher oil prices at least in the short term, inflation in the West (in blue for the Eurozone and green for the US) and in China (in orange) remained under control.

SOURCE : BLOOMBERG

SOURCE : BLOOMBERG

On the macro-economic front, there are still clouds on the horizon though, mainly the precarious state of government finances. The US government deficit remains concerning and the government is now expecting to spend close to USD 1.3 trillion on interest costs in 2026, consuming 15% to 18% of the total budget or more than 3% of GDP. Closer to us, Belgium and France also saw costs increase significantly in recent years. The Belgian government is now spending more than 2.5% of its GDP on interest costs and this share is expected to rise to close to 3% as the country raises debt at a higher cost.

This is why we hold to a global approach, and why we avoid instruments like long-duration sovereign bonds where the yield no longer compensates for the credit risk.

A Global Earnings Boom

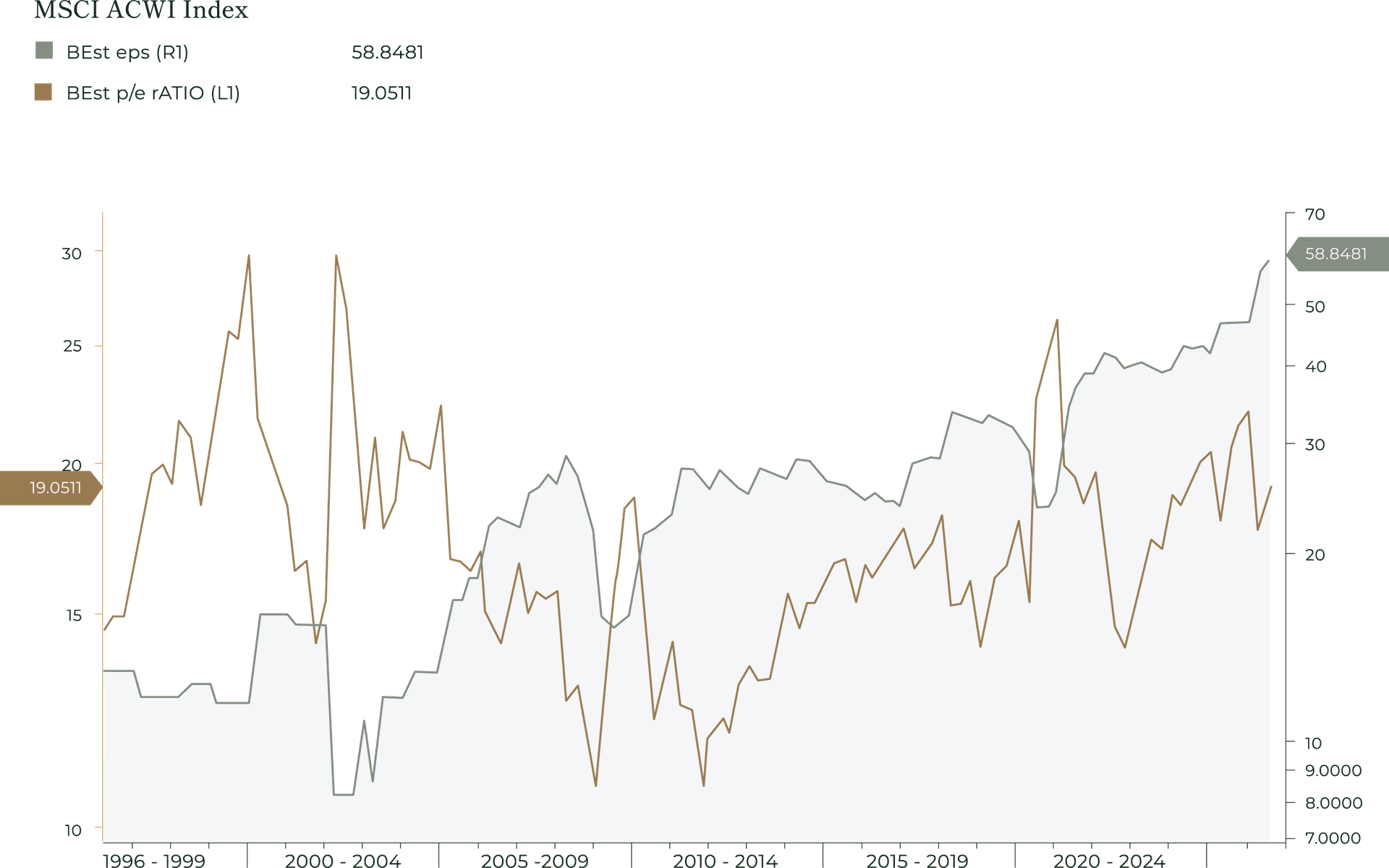

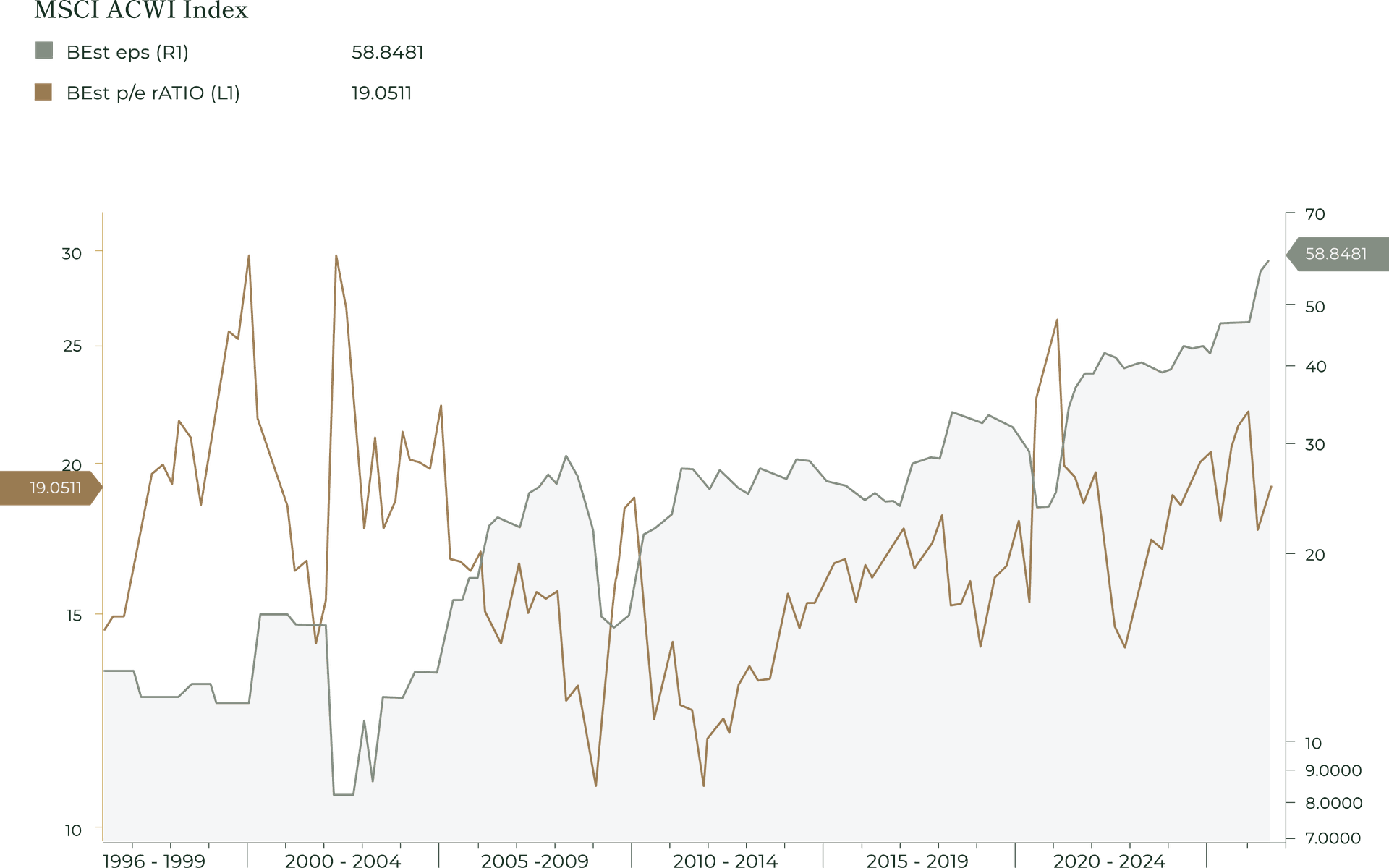

AN EARNINGS BOOM IS DRIVING GLOBAL EQUITIES

Global equities have not risen in a vacuum and contrary to what a lot of commentators might say, the overall stock market has de-rated, in terms of earnings multiples, in recent months.

As we can see on the graph below, listed corporate earnings per share (BEST-EPS2 in green below) have grown significantly in recent months and earnings valuation multiples, like the BEST-PE ratio in orange below, have gone down. The stock market is certainly not cheap, but it is far from the valuation levels of the internet boom times in 1999. As long as corporate earnings rise significantly, the stock market remains interesting for the patient investor.

² BEst-EPS: Bloomberg consensus estimate of forward earnings per share, aggregated daily from the forecasts of sell-side analysts. BEst-PE: the corresponding forward price-to-earnings ratio (index price divided by BEst-EPS).

SOURCE : BLOOMBERG

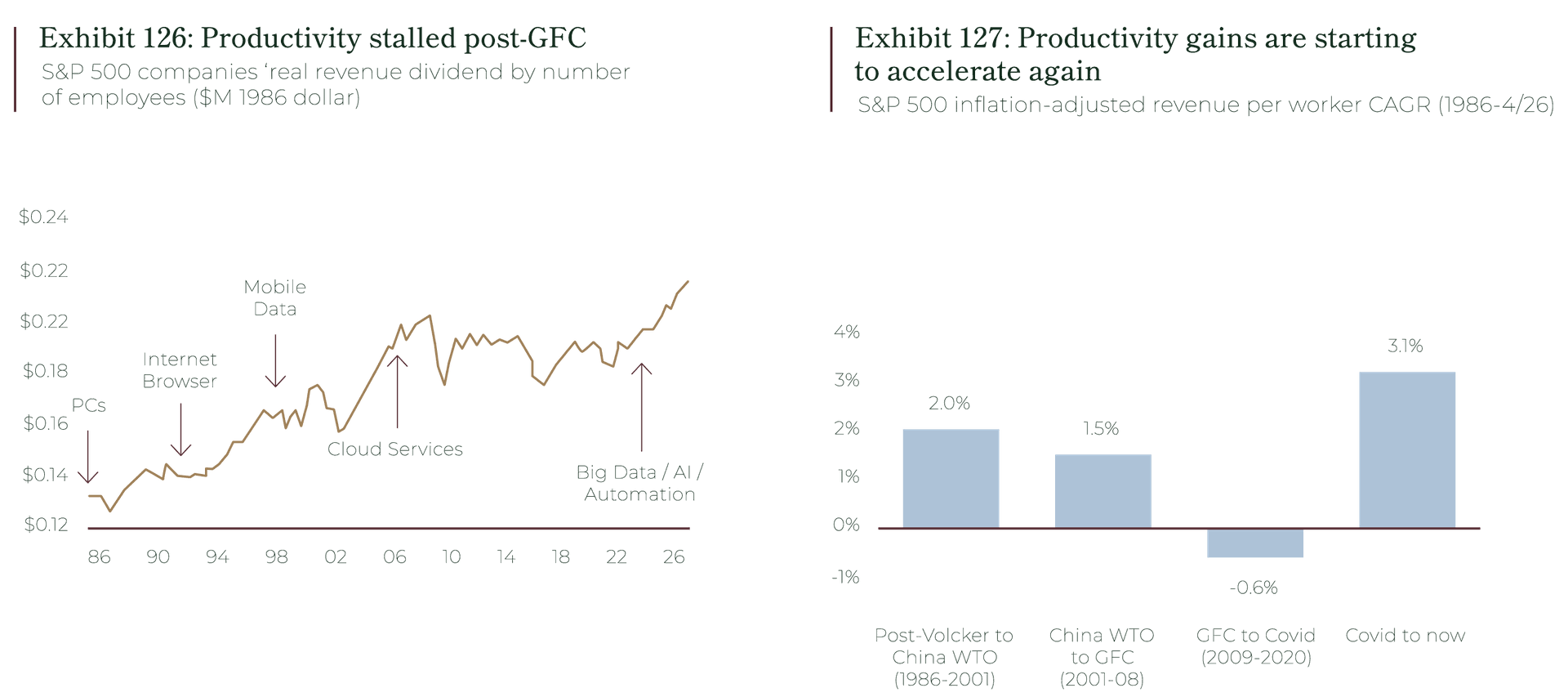

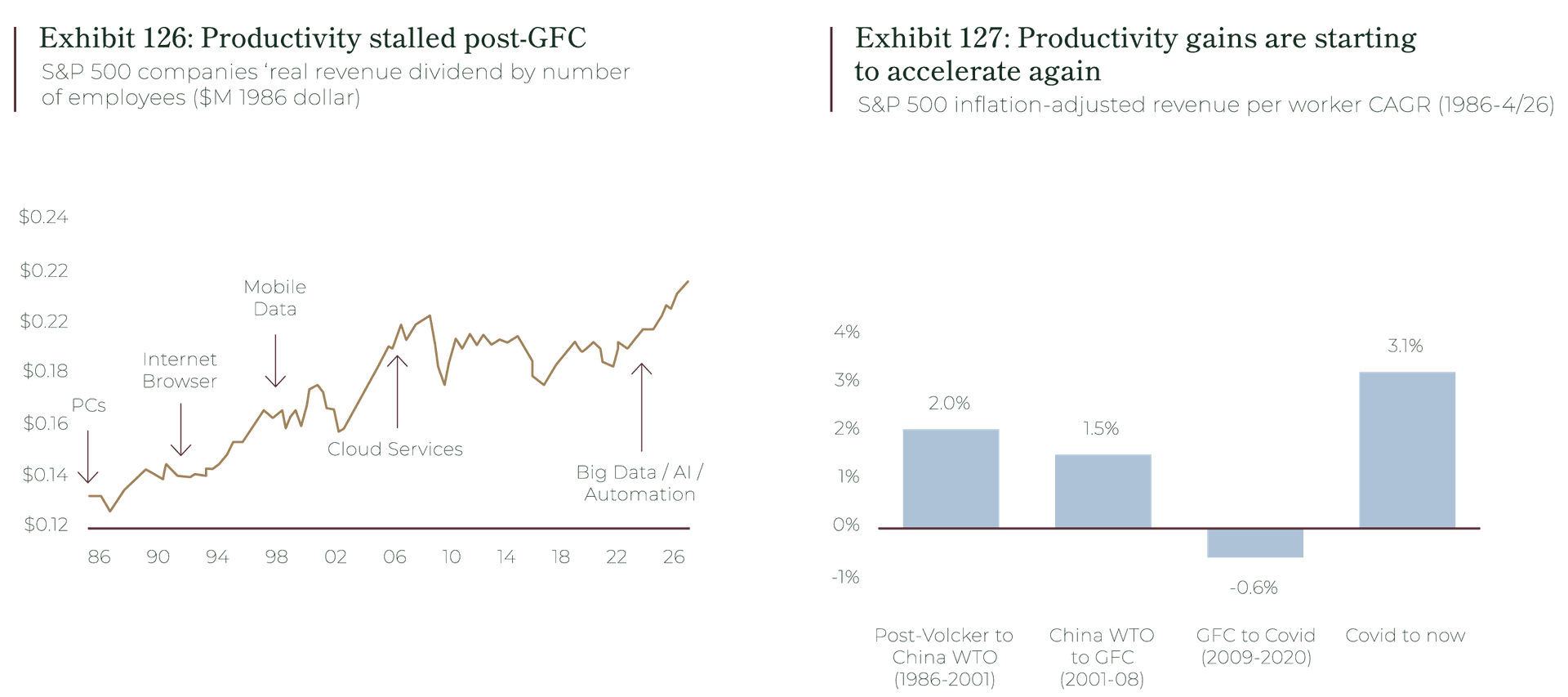

A lot of analysts are sceptical about the ability of companies to grow earnings from the current levels but we believe there is a very positive case to be made. Productivity, which measures the real economic output per worker has positively surprised in recent years, especially in the United States. The American investment bank Merrill Lynch recently observed, as shown on the two graphs below, that productivity increases at S&P 500 companies have rarely been as strong. In addition, the productivity boom started before the recent deployment of artificial intelligence and there is a good chance that productivity will keep rising. The Economist, in a recent article, wrote about this positive evolution and observed that the increase in productivity is spread across sectors, another positive for growth.

³ « America is experiencing a productivity miracle »

SOURCE : BLOOMBERG

SOURCE : BOFA US EQUITY & QUANT STRATEGY, FACTSET

SOURCE : BOFA US EQUITY & QUANT STRATEGY, FACTSET

While earnings rise and the global stock market performs well, we remain vigilant, trying to avoid bubbles and using the right strategies to maximise the risk-return potential for our clients. One major development we are following closely is the boom in artificial intelligence which is now affecting a vast number of businesses across the world.

THE INTERNET AND ARTIFICIAL INTELLIGENCE

Two major technological revolutions born in silicon valley

Valuations of the companies building and deploying AI have soared, capital expenditure plans run into the hundreds of billions, and the enthusiasm has the unmistakable feel of a technology gold rush. For anyone who lived through the late 1990s, the resemblance is impossible to ignore.

Both the internet and artificial intelligence are genuine, general-purpose technologies, the kind that reshape entire economies rather than single industries. Both attracted enormous capital on the promise of transforming how the world works.

This is the uncomfortable truth that the dot-com analogy reveals: the internet sceptics of 1999 were wrong about the technology and right about the valuations. The web did change everything. And yet the NASDAQ still fell roughly 78% from its peak, and it took fifteen years to reclaim that high. A revolution being real does not protect investors from paying too much to participate in it.

WHAT IS DIFFERENT TODAY

The differences between 1999 and today matter as much as the similarities, and they cut in both directions, some reassuring, some far less so.

Technology is everywhere and highly profitable. In 1999, many of the era’s darlings had no revenue, let alone profits. Today’s technology leaders are among the most profitable enterprises in history, generating vast, real cash flows. Companies with fortress balance sheets are building today’s AI platforms, not the speculative start-ups burning venture capital. This is a genuine and important contrast: the foundations are sturdier. One issue though, as we can see in the graphs below is that the free cash flow profile of these large American technology companies is quickly deteriorating with the American hyper-scalers now spending all their operating cash flow on AI data centres.

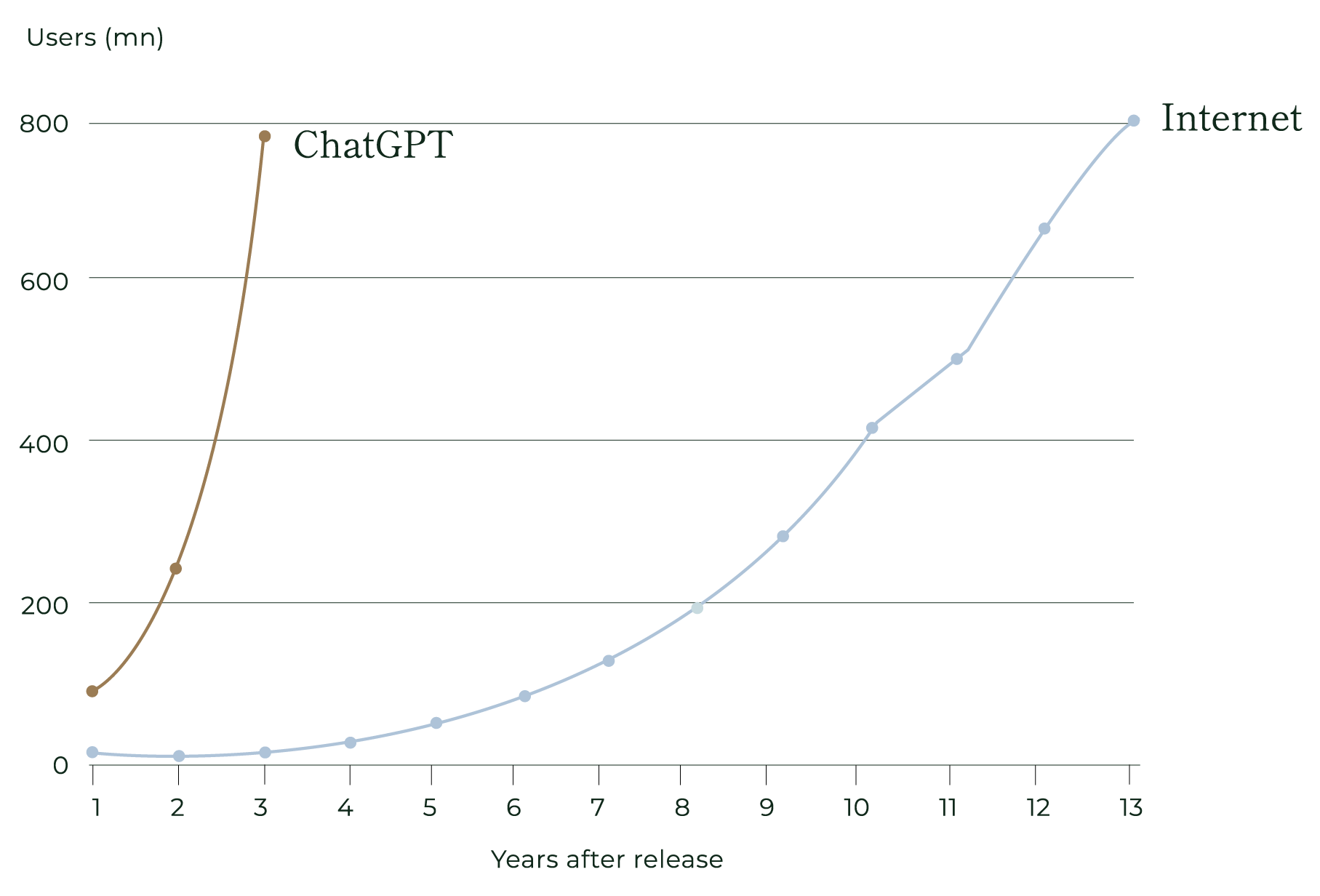

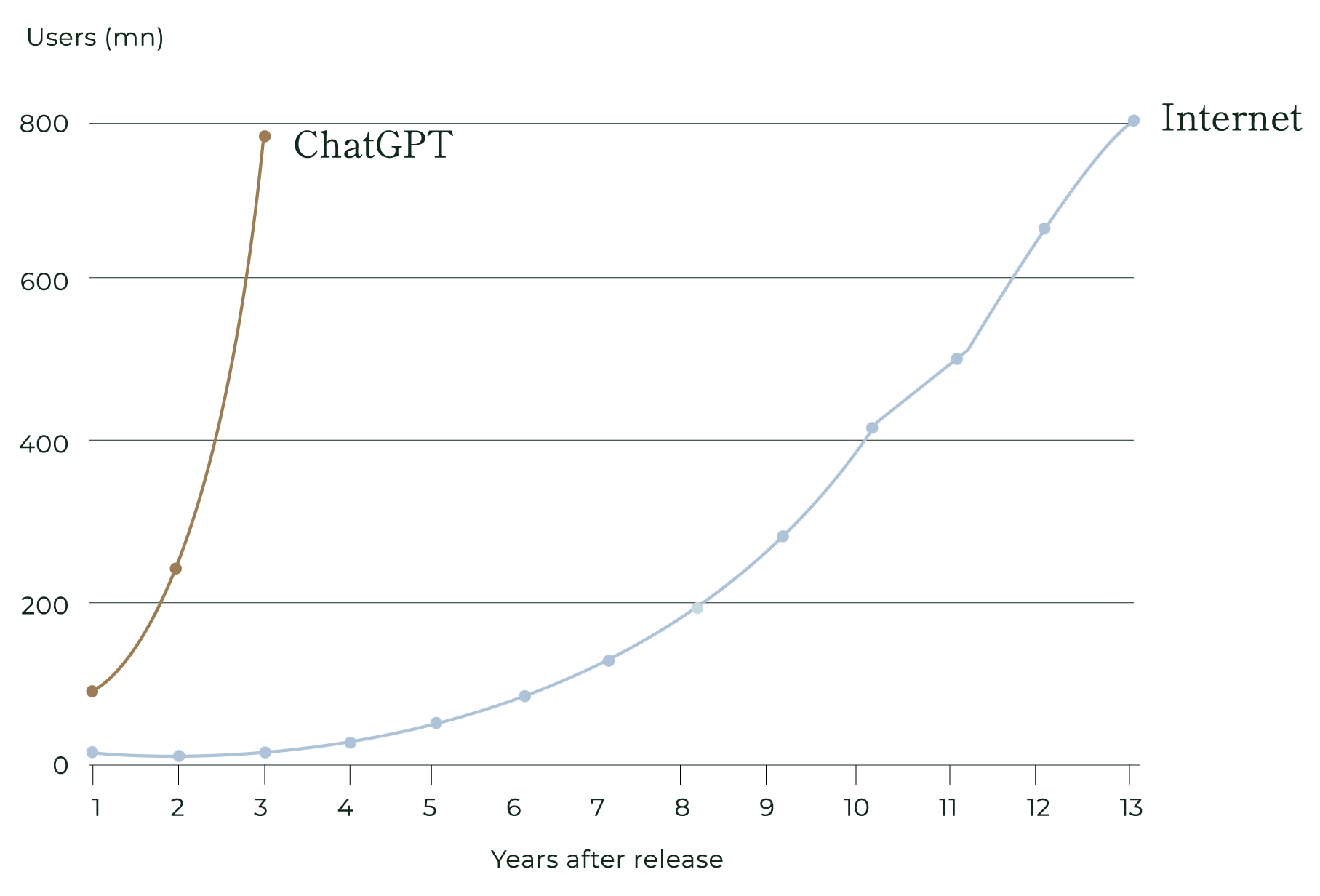

Everything moves faster. Adoption curves that took the internet years now take AI months. As the Financial Times observed recently, it took nearly 13 years for the internet to reach 800 million users, a number which was reached by ChatGPT in less than 3 years. Capital is raised, deployed, and repriced at a velocity that was unimaginable twenty-five years ago. Anthropic, the owner of Claude and one of the leading AI platforms, has filed confidentially for an IPO, following a funding round that valued the company at close to USD 1 trillion. It would make a five-year-old company one of the most valuable businesses in the world.

Speed cuts both ways: value can be created astonishingly quickly, but it can also be destroyed, and sentiment can reverse, just as fast.

SOURCE : FINANCIAL TIMES

SOURCE : FINANCIAL TIMES

Capital Allocation: The Danger of Bubbles and Bad Assets

« I can calculate the movement of stars, but not the madness of men. »

Isaac Newton

« I can calculate the movement of stars, but not the madness of men. » Isaac Newton

The term « bubble » in reference to financial crises can trace its origins to the British South Sea Bubble, a colonial enterprise promising vast riches to its investors. Interestingly, the world hasn’t really changed. Investors still fear missing the next big thing and even the brightest minds, like Newton who lost the equivalent of several million euros in the South Sea Bubble, can fail to resist the appeal of speculation. For a modern investor, the colonisation of Mars combined with artificial intelligence sounds as appealing as South American gold treasures for the 18th century British merchant.

DANGER OF OVERPAYING

Spacex and galactic exuberance

Few assets capture the mood of the moment better than the soaring private valuations of companies promising to remake entire frontiers, with space ventures the most vivid example. SpaceX has achieved genuinely historic engineering feats, and its commercial satellite business generates real revenue. Yet the valuations now attached to it, and to the broader cohort of space and frontier-technology companies, increasingly price in not just success but flawless, decades-long execution.

Traditional investors look at valuation multiples, like price-earnings, free-cash-flow yield or price-to-book when they analyse stocks. We are the first ones to admit though that these traditional methods don’t work very well for hyper-growth stocks, and sticking to them closely would have meant missing some of the best investments of the last decade like Tesla or NVIDIA. Now, arithmetic still matters. Buying an exceptionally well-managed company at very high multiples can still work if the absolute market capitalisation compared to the addressable market is reasonable. Simply put, if you pay millions or billions, you have a higher expected return than if you pay hundreds of billions or even trillions as in the case of SpaceX.

CHEAP IS NOT SYNONYMOUS WITH GOOD VALUE

« It is far better to buy a wonderful company at a fair price than a fair company at a wonderful price. »

Warren Buffett

« It is far better to buy a wonderful company at a fair price than a fair company at a wonderful price. »

Warren Buffett

Crucially, quality and fair value are not opposites, they are conditions that must hold together. Paying any price for a great business is a mistake; so is buying a declining business simply because it looks cheap. The discipline is to insist on both. In a market where the most fashionable names trade at valuations that assume a flawless future, the unfashionable but excellent business, fairly priced, is where we believe long-term returns are most reliably found.

Our Approach & Conclusion

Discipline in practice

Listed equities remain the asset class with the best asymmetric return potential. A stock can lose everything, like any financial asset. Unlike a bond, it can also multiply many times over. That asymmetry rewards discipline: we make sure we don’t overpay or buy bad assets. Our investment strategies follow three principles:

Invest globally across every sector.

Simple in theory, but more complicated in practice as a lot of global indexes now follow a similar narrative driven by the artificial intelligence boom. We look wider, on the principle that the best opportunities are rarely where everyone else is already looking.

Use a mix of valuation and quality criteria.

Several of our strategies mix valuation criteria like free-cash-flow, earnings growth and more custom factors like share-buybacks. The investment philosophy is to avoid over-priced securities and bad businesses.

Use a systematic approach.

The rise of computing power now allows investors to analyse thousands of data points very quickly and much faster than the human brain can do. Our systematic investment approach prevents psychological biases and can adjust very quickly to changes in market dynamics.

Invest globally across every sector.

Simple in theory, but more complicated in practice as a lot of global indexes now follow a similar narrative driven by the artificial intelligence boom. We look wider, on the principle that the best opportunities are rarely where everyone else is already looking.

Use a mix of valuation and quality criteria.

Several of our strategies mix valuation criteria like free-cash-flow, earnings growth and more custom factors like share-buybacks. The investment philosophy is to avoid over-priced securities and bad businesses.

Use a systematic approach.

The rise of computing power now allows investors to analyse thousands of data points very quickly and much faster than the human brain can do. Our systematic investment approach prevents psychological biases and can adjust very quickly to changes in market dynamics.

When I started my career in the early eighties, investors had very limited information and tended to hold a few stocks, which meant they were under-diversified and most often didn’t own the names with the best potential returns. Eventually, the industry moved to actively managed funds, a better solution but still expensive and in most cases underwhelming. The rise of indexation and passive investment over the last two decades finally gave the masses access to the overall performance of the stock market. While still attractive, the evolution of markets and the increasing concentration in American technology make us believe that indexing based on market capitalisation might not be the best approach in the next few years. Instead, we are convinced that a systematic approach based on fundamental criteria will give investors the best potential returns.

Dell technologies: a case study

Dell Technologies is an interesting example of how our investment strategies work. The company, famously started by Michael Dell selling customised computers out of his college dorm, has transformed itself into a software and hardware business ready for the artificial intelligence age.

Unlike other technology heavyweights, the market capitalisation of the company is in the hundreds of billions, not trillions, and the business generates massive amounts of cash and earnings. The stock was always present in global indexes but far too small to make a real difference. Our systematic approach spotted the name at the end of last year and we built a position; the business then accelerated significantly, and the stock ended the quarter as one of the largest positive contributors.

A note on patience

We have, over recent letters, reminded readers that those who panicked during the April 2025 tariff scare turned a temporary correction into a permanent loss, and that those who fled the Q1 2026 energy shock missed the recovery that followed. The lesson runs in the other direction too. Just as fear should not drive investors out at the bottom, euphoria should not pull them to chase the hottest investment themes of the moment, like space exploration or artificial intelligence.

« As always, try to avoid excessive excitement or fears when investing, stay patient and disciplined. »

« As always, try to avoid excessive excitement or fears when investing, stay patient and disciplined. »

We do not know whether the AI boom will prove to be 1999 or something gentler. What we do know is that every major episode of the last fifty years, the oil shocks of the 1970s, the crash of 1987, the dot-com bust, 9/11, the financial crisis of 2008, COVID, the 2022 inflation shock, the 2025 tariff panic, and the 2026 energy scare, was eventually followed by a recovery that rewarded patient, disciplined investors. The investors who suffered permanent damage were those who either sold in fear or bought in a frenzy.

Thank you for your trust.

We remain available for any questions.

Jacques Berghmans & Félix Berghmans

Legal Disclaimer

The information contained in this document is for general purposes and does not take into account the investment objectives, financial situation or specific needs of an investor. This document should not be given to a US investor (as defined in US regulations). This document is based on sources that TreeTop Asset Management SA (the “Company”) believes to be reliable and reflects the views of the managers of the Company. This document is for information purposes only and does not constitute investment advice or a product offering. The Company accepts no liability, directly or indirectly, for the use of the document information.

Data showing past performance and trends are not necessarily a guide to future performance or developments. Data & Information as of 30th June 2026.

TreeTop does not offer guarantee of result or performance.

Published by TreeTop Asset Management SA, a UCITS Management Company licensed pursuant to the provisions of Chapter 15 of the Luxembourg Law of 17th December 2010.